Embarrassment of riches Loan price surge puts CLO managers in a bind

The global loan market is experiencing a powerful rally. Prices have climbed sharply across leveraged loans. What once looked like a steady income opportunity has turned into a challenge for CLO managers who must now deploy large pools of capital in a very tight market.

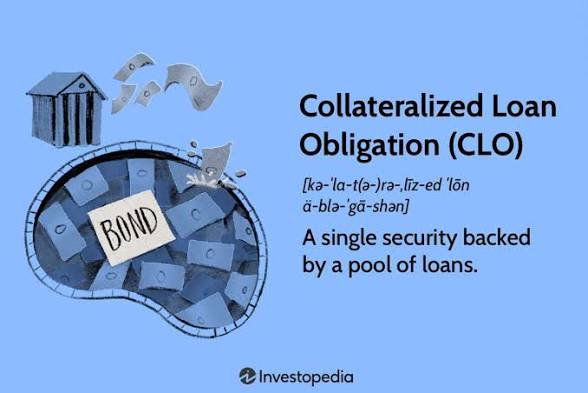

Collateralized loan obligations depend on buying diversified portfolios of loans. They earn returns by collecting interest from these loans. When loan prices rise too far the math becomes difficult. Managers struggle to find assets that offer enough yield to meet their obligations to investors.

The surge in prices has been driven by strong demand. Institutional investors are searching for income. At the same time supply of new loans has not kept pace. Companies are not issuing as much debt as before. This imbalance has pushed valuations higher and reduced attractive entry points.

For CLO managers this creates pressure on reinvestment strategies. Many existing portfolios are reaching reinvestment periods. Managers normally use this phase to replace maturing or prepaid loans with new ones. Now they face a market where most available loans are expensive and offer thinner returns.

Some managers are choosing to hold cash longer.

Others are turning to lower quality credits in search of yield. Both approaches carry risk. Holding cash reduces returns. Moving down the credit spectrum increases default risk if economic conditions weaken.

The situation also affects new CLO issuance. Investors are still interested in structured credit products but they are more selective. Higher loan prices mean tighter spreads which compress returns at the equity level of CLO structures.

Market participants describe the environment as an embarrassment of riches. There is abundant capital but limited opportunity. The abundance of liquidity is not translating into easy deployment. Instead it is creating a competition for scarce attractive assets.

Looking ahead CLO managers will need to rely more on active trading and credit selection. Small differences in pricing and structure will matter more than before.

The ability to source loans directly and negotiate in the primary market may become a key advantage.

If loan prices remain elevated the industry may see slower growth in new CLO formation. The balance between risk and return will continue to define strategy in this compressed market environment.